Law firms that are slow to adapt to the competitive pressures created by ALSPs may face an increasingly challenging legal market

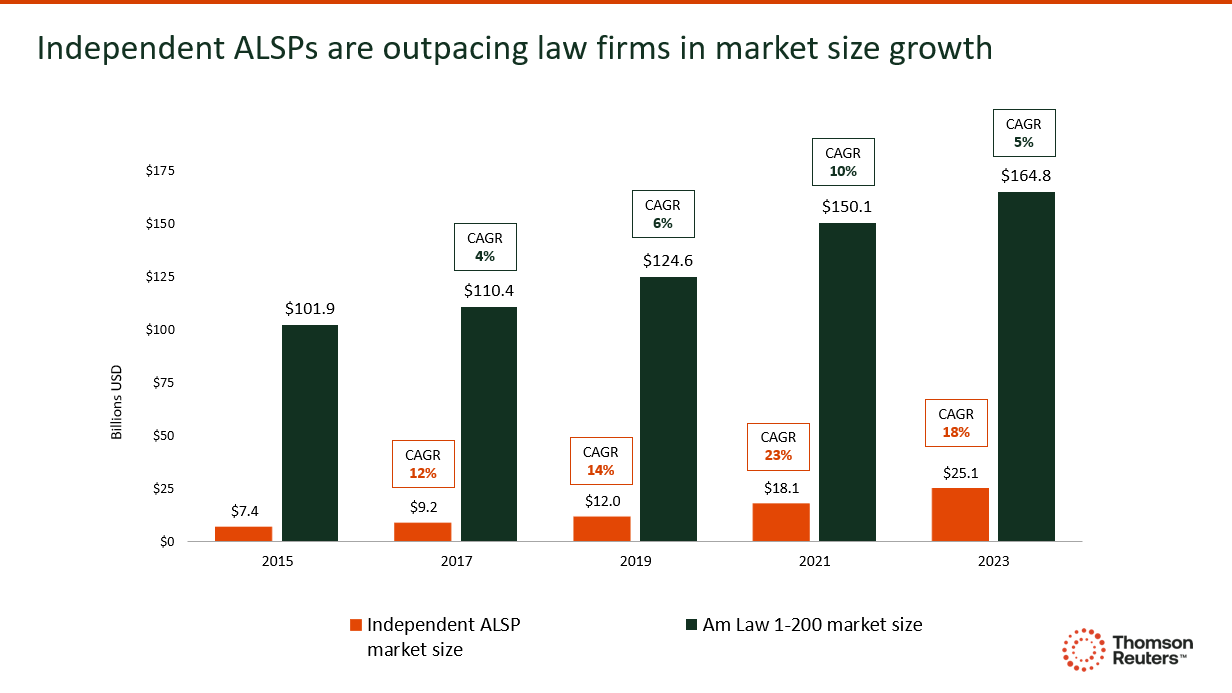

The independent alternative legal services providers (ALSP) market has expanded significantly, reaching approximately $25 billion by the end of 2023, according to the Thomson Reuters Institute’s recently published Alternative Legal Services Providers 2025 report. This marks yet another period of rapid growth, with a compound annual growth rate (CAGR) of around 18% from 2021 to 2023. Importantly, the report also extensively analyzes a growing bifurcation among law firms and corporate legal departments with regards to how they partner with and compete with these ALSPs. This last part — competition with ALSPs — deserves further discussion.

Are independent ALSPs and law firms competitors?

In the legal services universe, law firms have long been the go-to resource for individuals and companies seeking counsel. Their dominant position has allowed them to increase rates faster than other professional services and has resulted in some of the highest profit margins of any major industry. From 2015 to 2023, for example, demand combined with these rapidly increased rates to result in a roughly 6% revenue CAGR for firms in the Am Law 1-200 alone, easily outpacing broader economic growth in the United States.

This elevated top line growth, however, pales in comparison to the approximate 17% annualized revenue growth realized by independent ALSPs over the same period. As a result, and not surprisingly, law firms have lost legal service market share. By some estimates, law firms handled a little more than 90% of outside legal spend in 2015, but now that number is estimated to be closer to 86%. That four-percentage-point drop may not be much on its face; however, the pace of loss is accelerating and much of it is being absorbed by independent ALSPs. Yet despite this development, many law firm leaders said they do not see these providers as a threat to their business model.

|

|

Why law firms don’t see independent ALSPs as a threat

Of those law firm respondents surveyed in the ALSP 2025 report, only 21% said they believe that their traditional business model is being challenged by ALSPs. The other 79% are either unsure or disagree with the idea that ALSPs challenge their model. This perception rests on several key pillars, that include (not in order):

-

-

- A perception that law firms’ value proposition is fundamentally different than that offered by ALSPs

- A belief that ALSPs are taking work that would have been handled by in-house teams rather than outside counsel

- An expectation that current legal barriers will remain in place and continue to exclude independents from the work that law firms perform.

-

While these perceptions each have compelling arguments supporting them, there is a different perspective that exists as well.

Looking at independent ALSPs differently

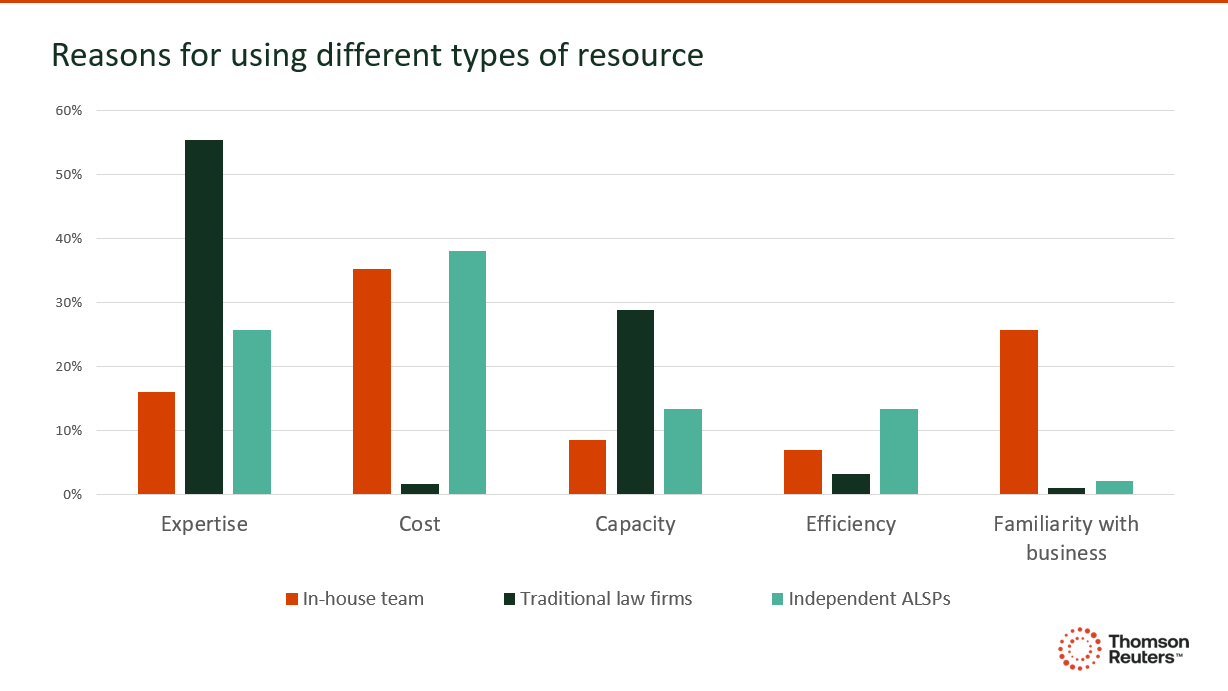

The first point mentioned above is connected to the fact that law firms currently have a corner on the most valuable area of legal service — legal advice. Corporate law departments surveyed in the ALSP 2025 Report did not anticipate allocating a significant, or even increasing, amount of their spend on legal advice toward independent ALSPs. This dominant market position on offering legal advice may suggest to law firms that the value they provide is unique. Indeed, in the chart below law firms lead by a substantial margin in the two areas upon which they focus: expertise and the ability to extend a law department’s capacity.

What this chart does not show is that over the previous editions of the ALSP report survey, we have observed a trend of independent ALSPs steadily encroaching on both of these value propositions. For instance, in the most recent survey we found that independents are rapidly becoming key players in the consulting services arena, which ranks as the third most utilized service after legal advice and support. This service area, far from being routine, demands a high level of expertise, and much of its growth is linked with advancements in technology, including software acquisitions and training. Independent ALSPs expertise is further evidenced by a noticeable decrease in concerns about the quality of services; as of the 2025 report, only 31% of respondents viewed quality as a barrier to using their services, down from 41% in 2021 (these data points also include affiliate ALSPs, however this broader trend of increased quality is applicable to independents specifically as well).

As for the capacity extension argument, the narrative that independent ALSPs are only absorbing work that law firms aren’t interested in is evolving. The 2025 report highlights a significant shift in purchasing behavior among corporate legal departments; they plan to reduce their reliance on legal managed services from traditional law firms while ramping up their spend on independent ALSPs. This pattern is also evident in matter-specific legal services. Such changes indicate that ALSPs are not merely complementary but are becoming essential partners for capacity expansion and strategic service delivery.

Only 21% of law firm respondents agree that their traditional business model is being challenged by ALSPs.

As for the third point — yes, laws in countries like the United States currently provide a regulatory moat for law firm’s top line. But is this moat sustainable, and more importantly, should it be depended upon? We already see examples of jurisdictions like the United Kingdom, Australia, and states such as Utah, Arizona and the District of Columbia that have either eliminated or lessened the restrictions placed on ALSPs towards the practice/business of law. While regulatory momentum has been slow in the US, recent initiatives from KPMG in Arizona, where the Big Four giant plans on starting a legal service business, highlights the potential for independent ALSPs in the legal advice niche and underscores the danger law firms could face if their moat is defined by regulation.

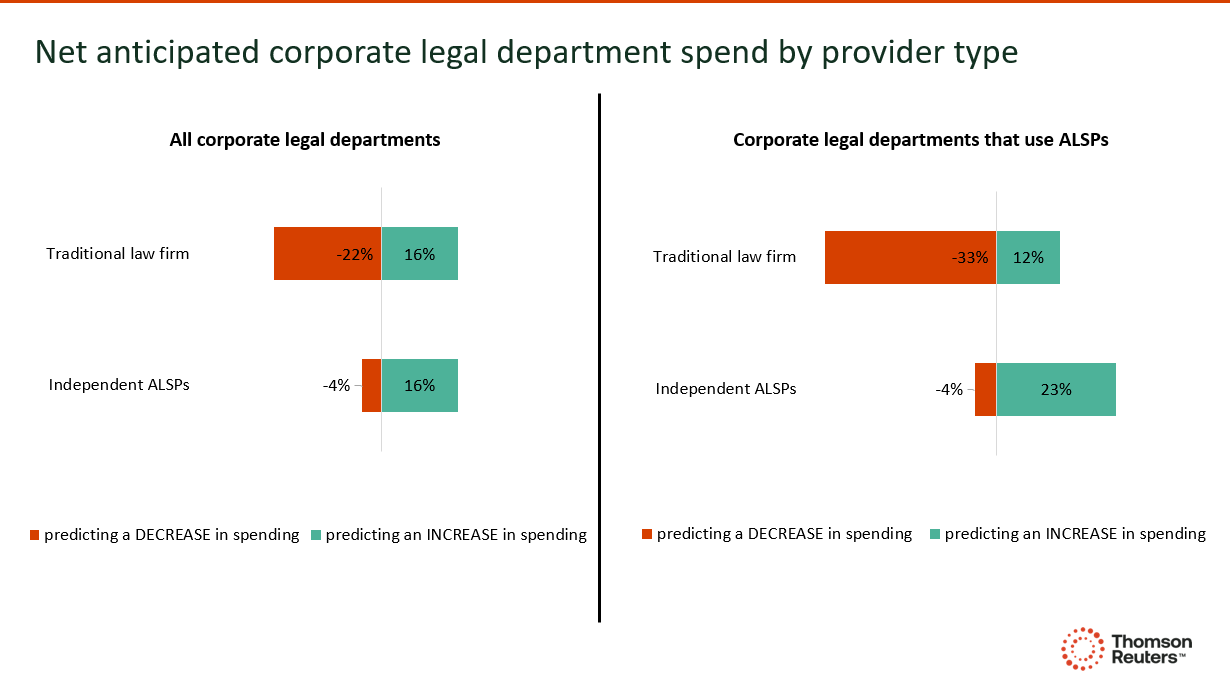

The threat of potentially shifting market landscape is further illustrated in the data below. Corporate clients are anticipating a greater amount of spend going towards independent ALSPs, while they intend to spend less on traditional law firms. Herein lies a critical insight: ALSPs are not just peripheral players but increasingly formidable competitors in the legal services landscape. Failing to recognize and adapt to this reality could result in further market share erosion for traditional law firms.

However, this competitive environment also presents an opportunity. Those law firms that strategically partner with third-party ALSPs or develop their own affiliate ALSPs can leverage these relationships to enhance their service offerings and remain competitive. Law firms must innovate and evolve beyond traditional practices to meet the changing demands of their clients. Embracing these shifts, rather than resisting them, will be essential for long-term success in an increasingly dynamic legal marketplace.