Law firms’ performance slid slightly in Q4 2024, and an important reason was that transactional practices were outpacing counter-cyclical ones in growth for the first time in two years

In the fourth quarter of 2024, law firms experienced a slowdown in performance, as indicated by composite score of the most recent Thomson Reuters® Institute Law Firm Financial Index (LFFI). That quarter marked the first contraction in the LFFI after seven consecutive quarters of growth, and for the first time since the Q4 2022, the LFFI actually decreased, dropping 7 points to reach a value of 64.

In Q4 2024, all the major metrics in the legal industry moved in the right direction in a year-over-year perspective. Demand accelerated 3.3% compared to Q4 2023, and worked rates and fees worked grew steadily 6.6% and 9.7%, respectively, during the same timeframe. In fact, the combined performance of demand and lawyer growth pushed productivity up 0.4% in Q4. While it would not be fair to say that these results are bad in any case, an increase in direct and overhead expense growth, as well as smaller gains in demand and productivity compared to previous quarters ended with many law firms seeing lower profit performance to close out 2024.

The shift between transactional & counter-cyclical demand

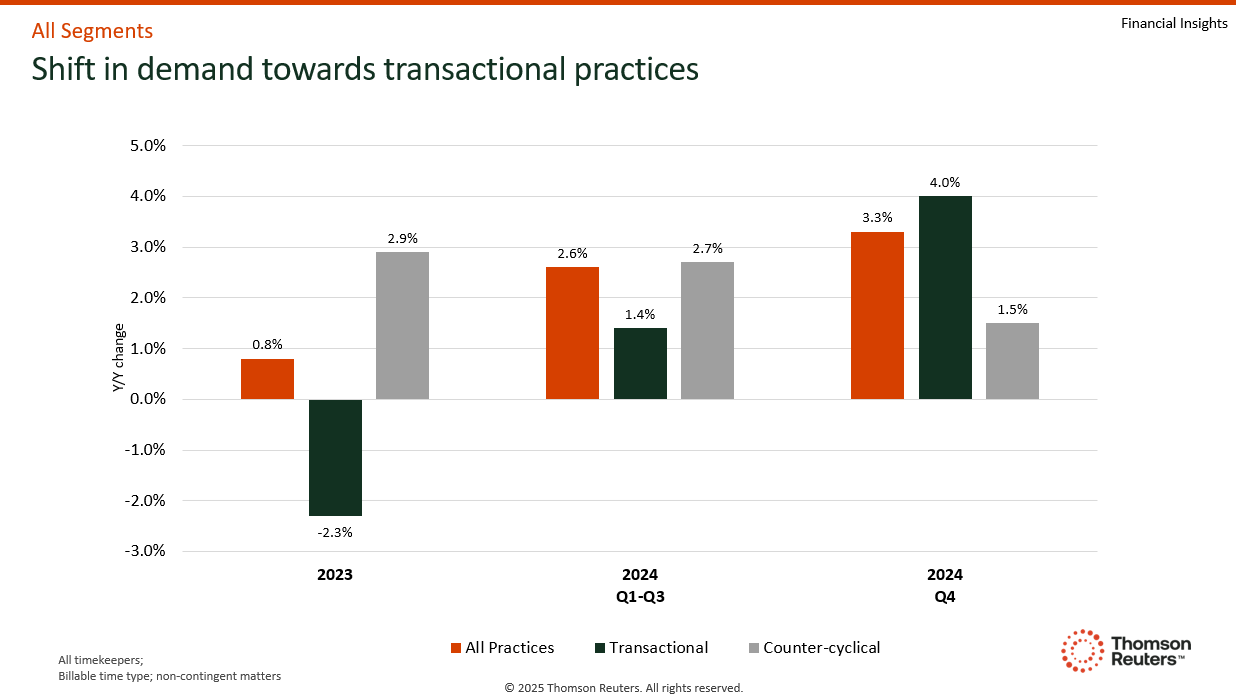

Early 2023 signaled the beginning of a new two-year trend in the legal industry that persisted until recently. This trend was characterized by a significant acceleration in demand for counter-cyclical practices, which tends to rise during slowdowns in normal business cycles and includes litigation, bankruptcy, and labor & employment practices. This counter-cyclical acceleration seemed to come at the expense of demand for transactional work, such as in corporate general, M&A, real estate, and tax practices.

During 2023, law firms averaged a 2.9% growth in demand for counter-cyclical practices, while experiencing a 2.3% decline in growth for transactional ones. This trend continued over the first three quarters of 2024, with counter-cyclical practices growing by an additional 2.7% on top of 2023’s strong growth. Meanwhile, transactional practices increased by just 1.4% year-over-year.

However, Q4 2024 reversed this trend, for the first time in years, exhibiting growth in transactional practices that outpaced that of counter-cyclical practices. While both practice types did experience growth — with transactional practices increasing by 4.0% and counter-cyclical practices by 1.5%, compared to the year-earlier period — the script had been flipped as corporate general, M&A, and real estate emerged as the top three fastest-growing practices in Q4. Interestingly, all transactional practices exceeded their year-to-date (YTD) growth levels in Q4 2024, while all counter-cyclical practices showed deceleration in Q4 compared to their YTD growth.

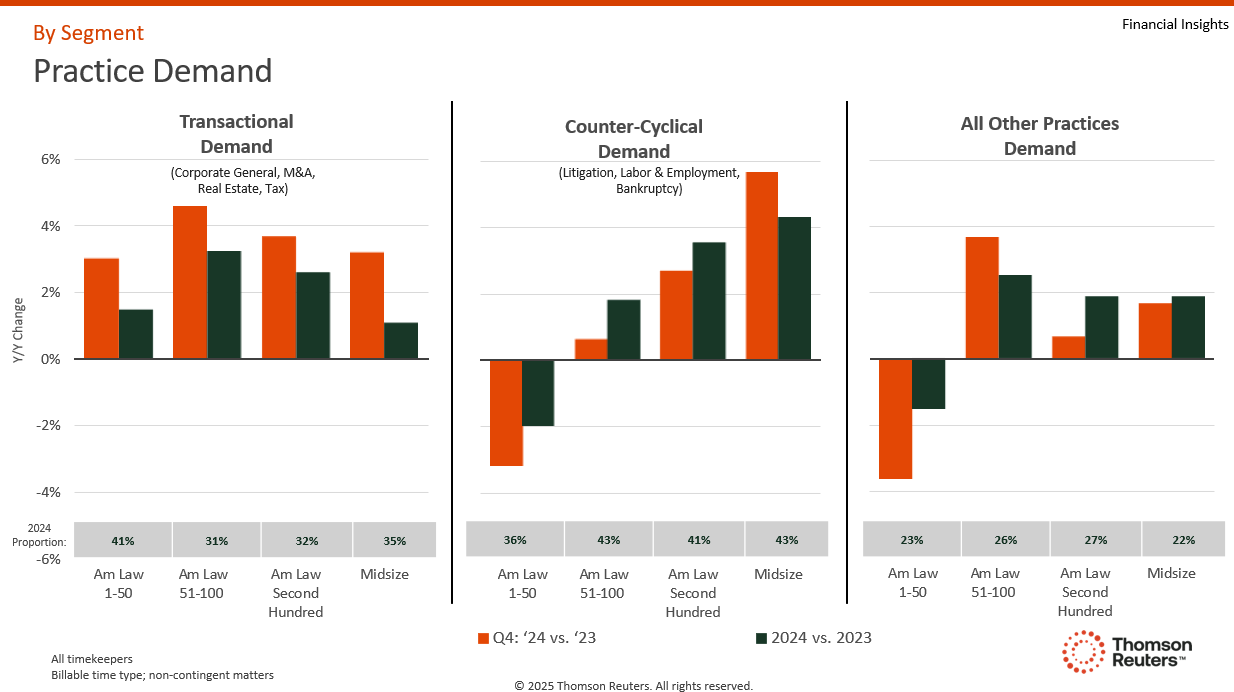

From a segment perspective, Q4’s transactional comeback was led by Am Law 51-100 firms, followed by Am Law Second Hundred firms, with the former averaging a 4.6% growth and the latter 3.7% in Q4, compared to Q4 2023. Midsize law firms increased their demand in these practice areas by 3.2%, while Am Law 1-50 firms saw a 3.0% increase. Apart from the Midsize segment, all other segments experienced a slowdown in their counter-cyclical growth in Q4, clearly showing the beginning of a trend in the overall industry.

What could 2025 hold for demand?

According to economists, expectations for the United States economy in 2025 reflect a solid labor market and strong consumer spending. However, while election-related ambiguity has been resolved, uncertainty from several perspectives still lingers. The new administration has introduced policy uncertainty regarding tax, regulation, immigration, as well as fears about potential trade wars. These policies could result in diminished GDP growth and additional pressures on inflation, which could also affect activity in the legal sector.

Our industry forecasting models powered by Financial Insights and broader economic data suggest a much more moderate growth environment for legal services during the first half of the year, primarily due to the disadvantages associated with working days and the strong baselines established in the previous year. While our models cannot predict the direction and impact of current political administration changes, history has shown that long-run growth typically dissipates quickly for the law firm market.

The level of the slowdown is still an open question. However, the shift of demand in which transactional practices surpassed counter-cyclical ones in Q4 2024 is expected to continue throughout 2025, our forecasting models suggest. In fact, some transactional practices — particularly corporate general — will likely continue accelerating throughout 2025.

On the other hand, counter-cyclical practices, such as litigation, might experience a deceleration in their growth rates compared to the previous year. A concern that arises from this scenario is whether the growth that is beginning to be seen in transactional practices will compensate for the potential slowdown in the counter-cyclical area. As a result — and in line with what our models are estimating — overall demand performance this year may be weaker than it was in 2024.

The deceleration of counter-cyclical practices can bring certain challenges in the near future, particularly for those law firm segments that have recently relied heavily on these practices to grow demand and revenue. Yet, considering the current administration’s aim to be more business-friendly, there could be more upside risks in the industry than our models currently foresee. In this sense, law firms should remain proactive and continue strengthening existing client relationships, enhancing operational efficiency, and investing in technology. Also, law firm leaders may want to seek opportunity in other geographic markets or practice areas in order to open additional revenue streams. This way, law firms will be able to navigate the challenges that 2025 could bring with remarkable success.

You can download the recent Q4 Thomson Reuters® Institute Law Firm Financial Index report here