As we begin the new year, we reflect on the changes the legal market has endured throughout 2020, including the drastic reduction in lawyer headcount in Q3

While Q1 showed how promising things can look in an undisrupted market, and Q2 reflected how quickly the legal market could adapt and prepare for an uncertain and disrupted future, the third quarter of 2020 portrayed a middle ground. A place where aggressive precautionary measures can be unwound and future growth plans can be put in place on sounder, albeit still uncertain, ground.

Demand continued its decline in the third quarter, down 2.4%, though representing a relative improvement compared to the 5.9% contraction in Q2. Law firms in turn began taking steps to mitigate losses, primarily with reductions in headcount and expenditures. Fewer lawyers and professional staff on the payroll lowered the cost of lost work in the third quarter, while the lawyers who remain returned to workloads that, while still lower, were more comparable to “normal” times. This dynamic was reflected in Thomson Reuters Peer Monitor’s productivity metric or data showing that the hours worked per lawyer contracting by a more modest 2.4% in Q3, compared to the whooping 7.2% in Q2.

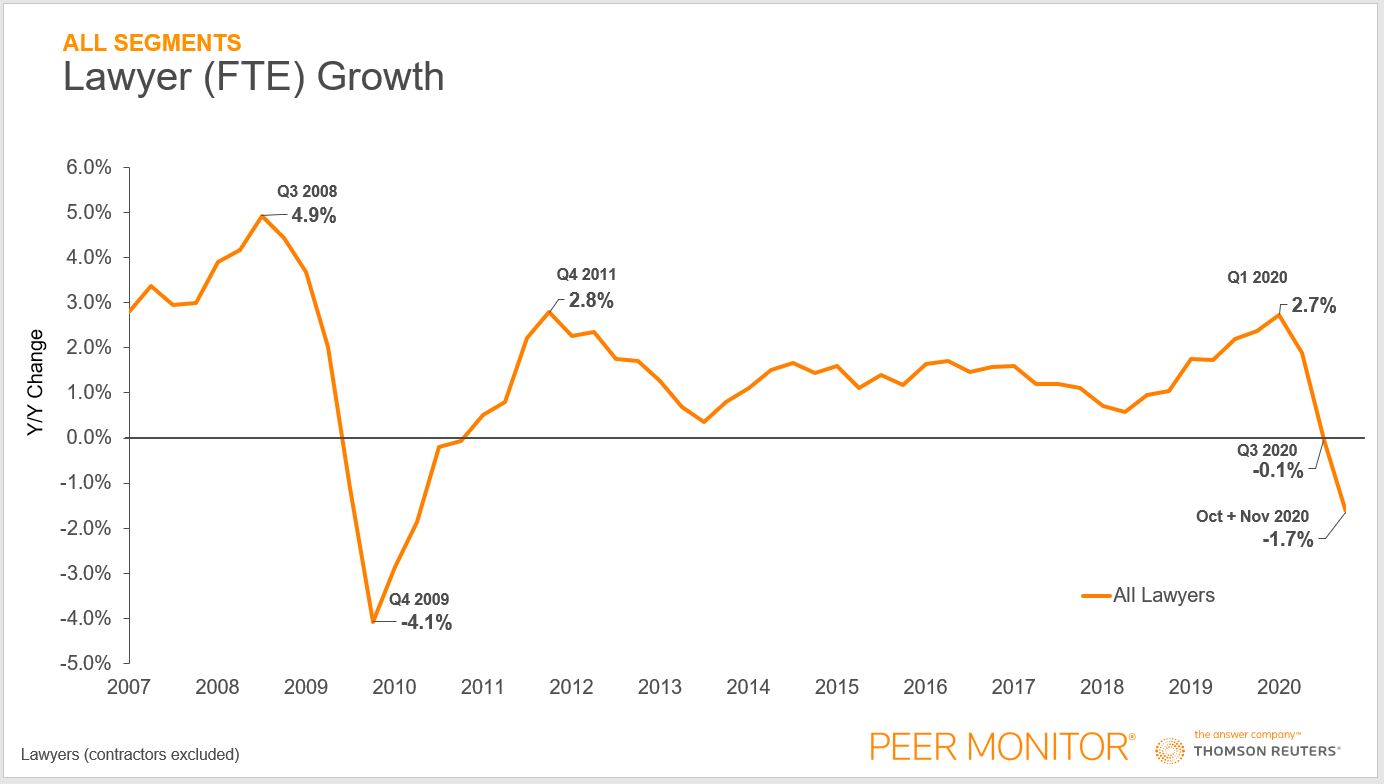

While many firms didn’t publicly announce any large scale layoffs or reductions of lawyers, results from Thomson Reuters’ Law Firm Business Leaders Report found that “under-performing lawyers” were the second-highest risk facing law firms cited by survey respondents. Further, Altman Weil’s 2020 Law Firms in Transition Survey reported that 84% of firms have chronically under-performing lawyers. With that in mind, we can see how our lawyer (FTE) growth chart below reflects a market where the average law firm reduced lawyer headcount by 0.1% in the third quarter.

This troubling statistic was the first time this metric had contracted since the beginning of the Great Recession of 2008-‘09. Not surprisingly, this trend continued into October and November of 2020, where headcount reductions stand at nearly 2% on average.

Looking back at 2009 — the last time law firms contracted their lawyer headcount — is illuminating. At that time, law firms were coming off a growth peak (in Q3 2008) that was nearly twice the pace at which firms were hiring in Q1 of 2020. Also, the ensuing contraction low (in Q4 2009) came a year or so later.

It would be naïve at best to say these two recessionary periods in lawyer growth will have similar extents of decline or length of contraction, but it is difficult to imagine firms returning to hiring in the first quarter of the new year.

Indeed, it’s still worth pointing out that firms quickly ratified a majority of the headcount reductions in the 2008-‘10 range. In Q4 2011, two years after the market’s low, law firms grew headcount at 2.8% on average. That peak hasn’t been topped since, which reflects an overall sense of regret for the over-the-top cutbacks during the Great Recession and ensuing economic crisis. Clearly, this is something that is sure to be on the minds of law firm management as they continue in the current crisis.

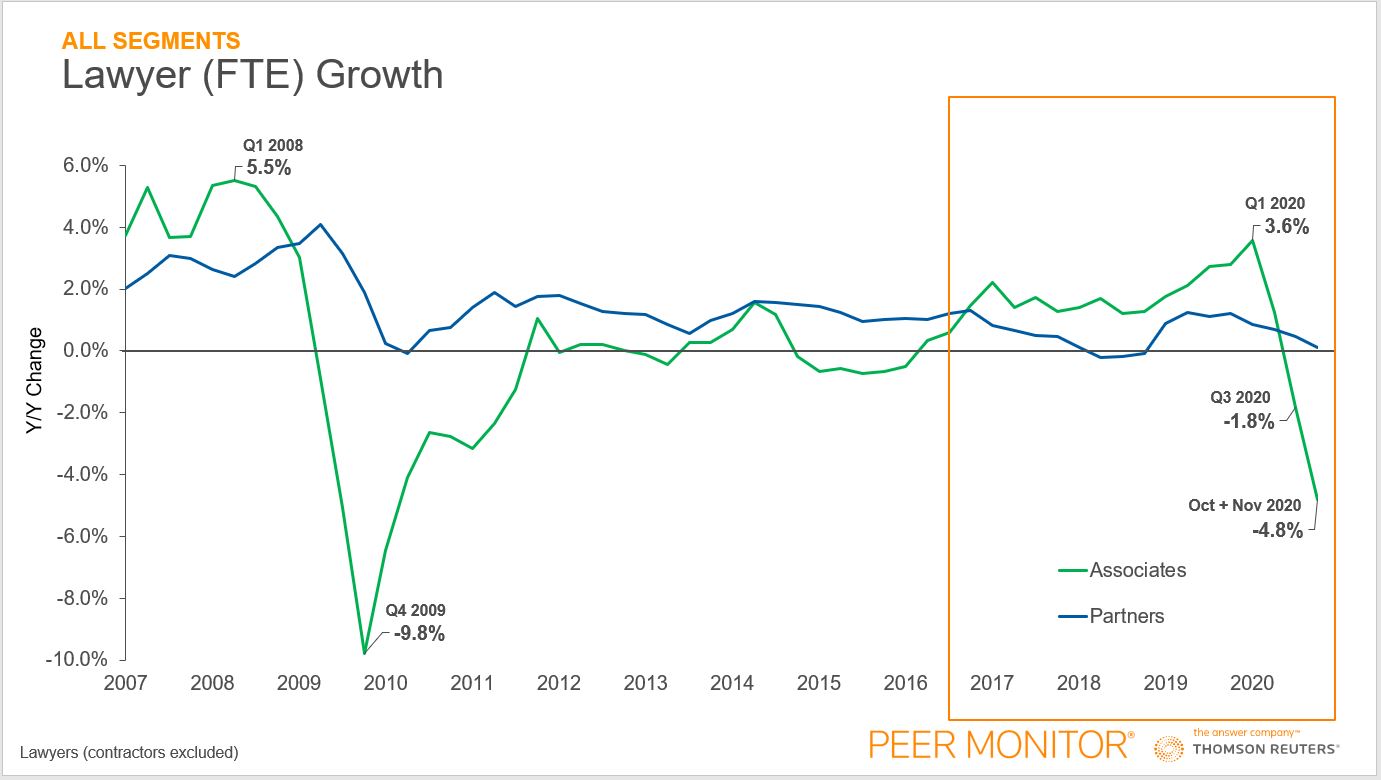

What has been similar about the headcount reductions in the past and today, comes from how associates have experienced the brunt of these attorney cutbacks. In the fourth quarter of 2009, each firm on average employed nearly 10% fewer associates than they did in the year-earlier period (Q4 2008), a staggering figure. Firms have been trying to replenish those “lost” associate classes ever since, and they have struggled to do so until 2017, when the “Great Associate Pay Raises” became much more widespread.

From 2017 to the beginning of 2020, associate class levels have grown at a much faster rate than any other lawyer title during this time. This reached a peak of 3.6% in the first quarter of this year, a pace that hadn’t been seen since before the Great Recession. If law firms took the time during the second and third quarters of last year to scrutinize each and every lawyer in their firms based on their performance to see if they are under-performing their pay, it would make a lot of sense that Associates as a class would be reduced at a much faster rate than the partners within the firm.

In addition to the floor-raising pay raises in recent years, most associates don’t carry the relationships or clients needed to maintain billable hours goals during demand downturns, especially during the COVID-19 pandemic, where unprecedented uncertainty drove clients to seek out their most trusted partners during the early months. Along those same lines, reducing partners could take much more revenue and fees away from firms’ balance sheets, if their clients remained loyal to those ex-partners. And this doesn’t even touch on the politics or internal issues that are at play with these types of headcount-reduction decisions, which have tended to be a positive for partners. Indeed, partners’ average headcount growth has never contracted more than one-half a percent in a single quarter over the 13 years shown above.

It is strongly evident that law firms reacted quickly to the near-term effects that the COVID-19 pandemic, just as firms had during the previous global financial crisis. While the reasons behind these trends may be radically different, both results end with firms reducing their “underperforming” lawyers, who often tend to be of the associate class.

Those actions have resulted in 2020 profitability metrics that measure up extremely well given the circumstances. What remains to be seen is to what extent these cuts will continue and for how long; however, it’s hard to believe that firms will make the same mistakes that cost the law firms for years following the last crisis. Indeed, as now-thinner associate classes have begun to emerge, it will no doubt effect succession planning and leverage modeling within firms.

And those law firm leaders who combat these issues of the past effectively today will separate their firms from the pack in 2021 and beyond.

You can download the 2021 Report on the State of the U.S. Legal Market here.