Tax firms are shifting strategies by emphasizing efficiency, talent, and client services to promote their own sustainable growth

According to the Thomson Reuters Institute’s recent 2024 State of Tax Professionals Report, it may appear that tax firms are de-prioritizing growth in favor of other priorities… but the reality is a little more nuanced.

The Tax Professionals Report, for which more than 500 tax firm professionals were surveyed from accounting firms across the globe, showed that about 19% of respondents listed firm growth as their number one priority, which was down ten percentage points from the previous year. Interestingly, a report by Accounting Today showed that accounting firm revenues were down by one-third from the previous year.

For context, tax & accounting firms reached a record 19% annual revenue growth in 2023, the highest in decades. So, it’s worth a closer look at these two data points to determine what, if any, is the correlation and potential trends.

The obvious should be stated: Accounting firm leaders are very interested in growth. Even though it ranked fourth among the top priorities cited by respondents in the Tax Professionals Report, that doesn’t mean firm leaders are no longer interested in increasing profits and growing their businesses. Rather, tax firm leaders appear to be adopting a more strategic approach to growth, emphasizing efficiencies, automation, talent acquisition, and client services as their primary focus areas.

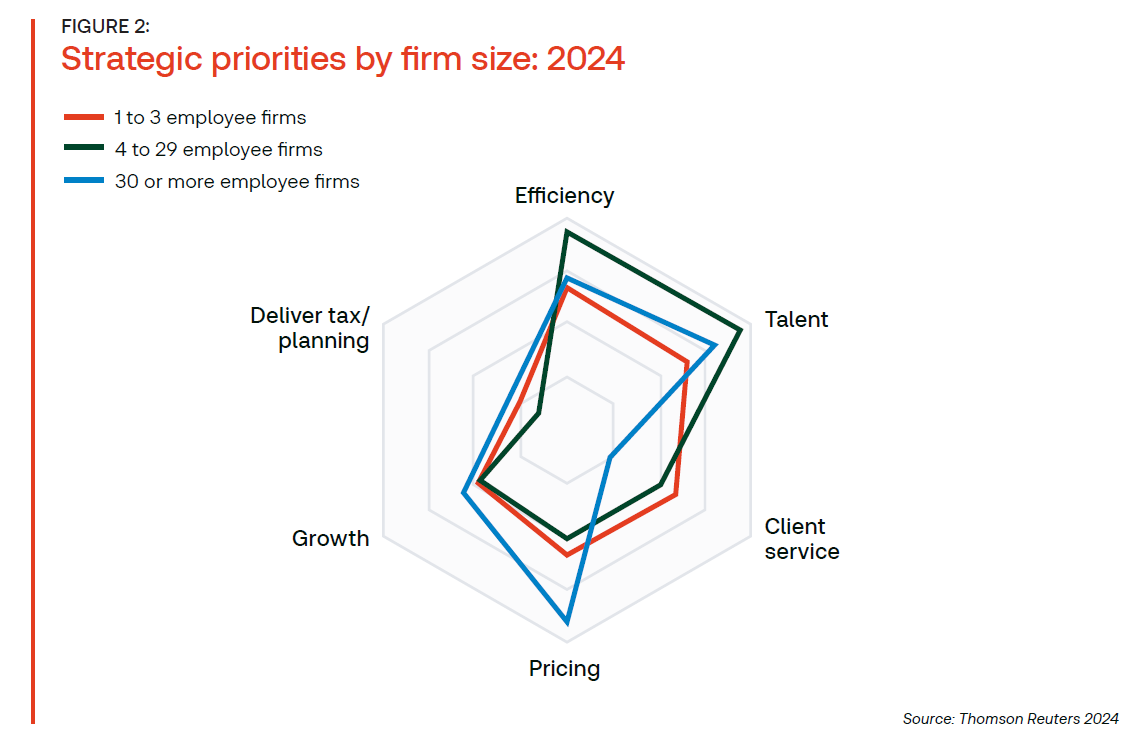

Efficiency to support growth

Improving efficiencies and expanding automation have taken the forefront as the number one priority for many tax firms. This trend is likely driven by the increasing complexity of tax regulations and the need for firms to streamline their operations in order to remain competitive. By investing in automation technologies, firms reduce the time their professionals spend on manual processes, while minimizing errors and improving overall productivity. This shift not only enhances operational efficiency but also allows firms to allocate resources more effectively towards higher-value activities, such as client advisory services.

In considering efficiencies, cost reduction is an important facet. Firm management teams should often review their current business strategy process, technology, and people utilization to determine where efficiencies and cost reduction could be found. Who is doing what, and with what? How long does it take? Is the current technology being fully utilized, or should it be improved or replaced?

Streamlining and scalability often can be the bedrock of efficiency. Leaders need to determine the tasks that can be systemized and whether automation should be incorporated to manage and improve accuracy and speed.

Talent: Reskilling and retention

The demand for skilled tax professionals has intensified, and firms are investing in strategies to recruit, develop, and retain their workforce. This includes providing ongoing training and development opportunities, and fostering a positive work environment that promotes employee well-being and job satisfaction. Indeed, many firms reported that their talent strategy was a central part of their growth, according to the Accounting Today report.

The talent piece is critical to firms today as they combat the challenges that the industry is facing, such as the shrinking number of students going into the accounting profession on top of the significant number of professionals leaving. And by training current employees while fostering a greater reliance on outsourcing, firms had potentially stretched their talent investments further.

Enhancing client services

Tax & accounting firms of all sizes continue to recognize that their business models have shifted from compliance-only work to fuller advisory services, and many firms have become intentional about what higher-value services they offer to clients. In an increasingly client-centric market, firms are focusing on delivering exceptional service to better differentiate themselves from competitors. This involves understanding clients’ unique needs, providing personalized solutions, and maintaining strong relationships.

For example, firms are increasing their approach to being industry-specific or focused on certain kinds of service offerings — from tax planning to business consulting. Over the years as tax firms evolved their businesses away from compliance and towards advisory, they had to focus on the business services that were strategically important to clients, while deciding what type of clients they wanted to engage. These could be clients from specific industries, such as construction, nonprofit, and manufacturing. By prioritizing specific client services, firms can enhance client satisfaction, foster loyalty, and drive long-term business growth through referrals and repeat business.

Other considerations for growth

The trend in non-organic growth continues. Mergers with competitors and investment from private equity firms both remain a stable pathway to growth for many tax & accounting firms. For many firms, M&A can seem an idyllic solution, allowing the firm to hit levels of growth on many fronts, including acquiring much-needed talent, expanding in a desired market or industry, and, of course, accessing a wider, larger client base.

Private equity firm investment, which once seemed more controversial among tax firms because of its potential to change firms’ structure, now are becoming more acceptable. Firms are recognizing the opportunities provided by such funding, including the ability to scale up quickly and purchase the necessary technologies to work more efficiently and be more competitive.

Overall, today’s tax & accounting firms are appearing to take an eagle-eye approach to their growth strategies. In doing so, their approach is to look to every aspect of the business from efficiencies to talent to client service and determine what and how growth should be promoted. By adopting this holistic and strategic approach to growth, firm leaders ensure their firms remain competitive and capable of navigating the evolving tax industry landscape.

You can download a copy of the Thomson Reuters Institute’s recent 2024 State of Tax Professionals Report, here.